Q1 Storage Prices Soar: DDR and SSD Double, Triggering a Scramble Among PC Manufacturers

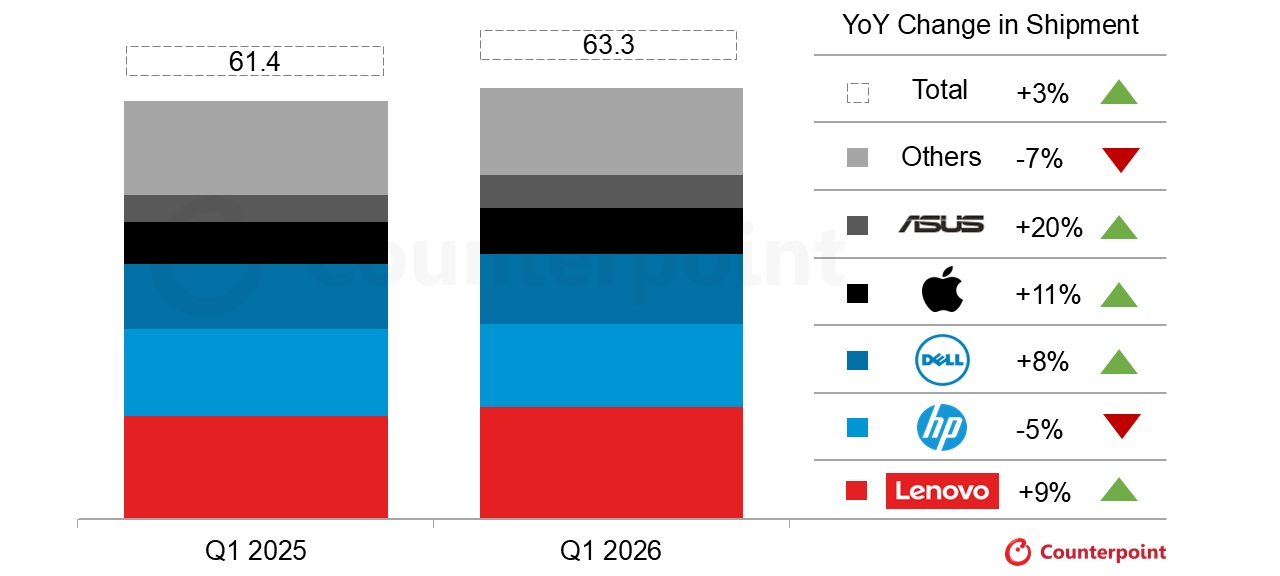

Counterpoint's latest report shows global PC shipments grew 3.2% year-on-year in the first quarter of 2026, reaching 63.3 million units. However, this "growth" is driven by a surge in memory and SSD costs leading to advanced stocking, rather than a natural recovery in demand.

The report points out that global PC manufacturers significantly increased their procurement of memory and SSDs in Q1 to lock in key component costs before comprehensive price increases at the terminal end, while also responding to the rigid replacement demand brought about by the end of support for Windows 10. Leading brands such as Lenovo, Dell, Apple, and ASUS all achieved shipment growth and further increased their market share, with ASUS and Apple experiencing the most significant increases of 20% and 11% respectively. Lenovo and Dell recorded year-on-year growth of 9% and 8% respectively. In contrast, HP's shipments declined by 5% year-on-year, and other small and medium-sized brands collectively declined by 7%.

Specifically, Lenovo continues to maintain the first position in global PC market share, with Q1 shipments increasing by 9% year-on-year to 16.5 million units, representing a market share of approximately 26%, a new high for the first quarter of any year. Although HP experienced a decline, it still maintains a leading position in the "second tier" ahead of the third-ranked manufacturer. Dell benefited from replacement demand in the commercial market, achieving 8% year-on-year growth. Apple, thanks to the availability of new MacBooks starting in March, saw its Q1 shipments increase significantly by 11% year-on-year to 6.7 million units. Counterpoint believes that with the full ramp-up of new models, Apple's growth momentum in the PC market will continue into the next quarter. ASUS, driven by strong demand for consumer-grade laptops, recorded a 20% year-on-year increase, with shipments reaching 4.8 million units, making it one of the best-performing brands this quarter.

The core variable supporting this round of concentrated stocking is the sharp rise in memory prices. Counterpoint's data shows that the price of entry-level 8GB DDR4 memory increased by 110% quarter-on-quarter in Q1, while the price of a 1TB entry-level SSD without cache (without DRAM) soared by 147%, with higher-end products experiencing even greater increases. The research firm expects DRAM prices to potentially rise another 60% in the coming months, and SSD prices to rise another 50%, with the specific magnitude depending on the type and specifications of the product. Against the backdrop of continued expansion in AI infrastructure investment, the constant demand from servers and data centers for key components such as DRAM and NAND continues to push up overall supply chain costs, and other PC core components such as CPUs are also expected to be affected.

Microsoft's promotion of Windows 11 and the Copilot+ ecosystem has also further stimulated the hardware update pace of PC manufacturers. To meet the new requirements of AI functions for computing power, memory, and storage bandwidth, chip suppliers and OEMs have simultaneously launched a number of new models aimed at "AI PCs," which has provided support for shipment data in the short term, but also squeezed the living space of traditional "high-value" models in a high-cost environment. The report points out that, with memory and SSD prices showing no signs of falling, manufacturers are forced to shift towards mid-to-high-end product structures to maintain profitability, which will test their supply chain management capabilities and product portfolio adjustment speed.

Counterpoint's "Memory Price Tracker and Forecast" market report further warns that PC memory prices nearly doubled in the first quarter of 2026 compared to the previous quarter, and this upward trend will continue in the second quarter, albeit with a slight slowdown in the rate of increase. The continuously rising costs will ultimately be passed on to the terminal market through whole machine prices, which will have a "significant negative impact" on the overall growth of the PC market in 2026. The report predicts that branded whole machines, relying on large-scale procurement and supply chain bargaining power, will still have the opportunity to maintain moderate growth, but the DIY assembly market has already shown obvious signs of cooling.

Given that there is "no sign of any fall in memory prices" in the short term, Counterpoint believes that there is a risk of the entire PC market re-entering a downward range from the second half of 2026 to early 2027. As mainstream price segments are continuously pushed higher, a large number of price-sensitive users may be forced to postpone or abandon upgrades, and the competition between PC manufacturers regarding supply security, product positioning, and pricing strategies will further intensify.