Chaos of Bundling Payment with Lending Will Be Rectified

According to Xinhua News Agency, on April 24th, the People's Bank of China and eight other departments jointly issued the "Administrative Measures for Online Marketing of Financial Products" (hereinafter referred to as the "Measures"), which will officially come into effect on September 30, 2026. Specifically addressing the chaos of embedding payment with lending in non-bank payment institutions, Article 12 of the "Measures" draws a clear red line: non-bank payment institutions shall not include financial products such as loans and asset management products in payment tool options, nor shall they provide marketing services for such financial products.

This regulation directly addresses the long-standing industry malady of deeply bundling payment with lending, not only standardizing the logic of payment scene display but also cutting off the financial marketing monetization path, together constituting a systemic constraint on the financial business model of payment institutions.

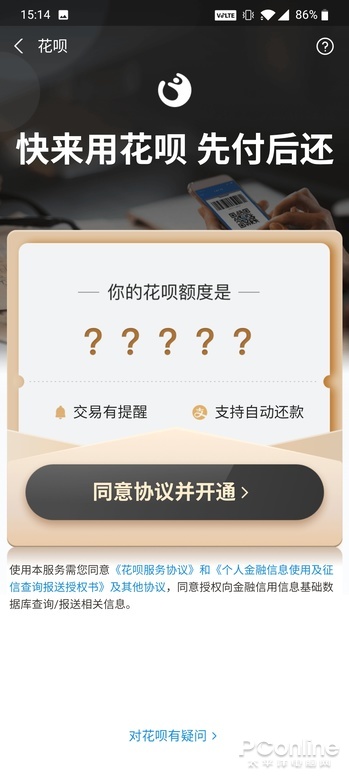

For a long time, in daily consumption scenarios such as e-commerce, food delivery, travel, and bill payment, credit installment products such as "Huabei," "Baibao," and "Monthly Payment" have often been displayed alongside conventional payment tools such as bank cards and account balances. Some platforms even engage in operations such as default selection, pop-up pushes, and pre-positioning recommendations, causing users to unintentionally activate or use credit services.

In response to the above-mentioned chaos, the "Measures" specifically regulates the content and behavior of financial online product marketing.

According to the "Measures," payment tools on the checkout page of payment institutions must be displayed separately from and prioritized over financial products such as loans, and options with similar wording such as "discount payment" or "installment payment" shall not be used to confuse payment tools with loan products.

At the same time, credit marketing rhetoric has been comprehensively tightened. Loan products shall not use marketing rhetoric such as "low threshold," "instant disbursement," or "low interest rates." For installment payments, consumers shall not be induced to consume by unilaterally promoting the preferential first-installment fees.