U.S. AI User Survey Reveals 80% of Wealthy Individuals Use Claude

A survey by EpochAI and Ipsos shows that 80% of Claude’s weekly active users in the U.S. come from households with an annual income of over $100,000. AI assistants are becoming stratified by price, access, and work scenarios, with high-income users being the first to access higher-tier AI services. A national U.S. survey has revealed differences in user profiles among major flagship large language models.

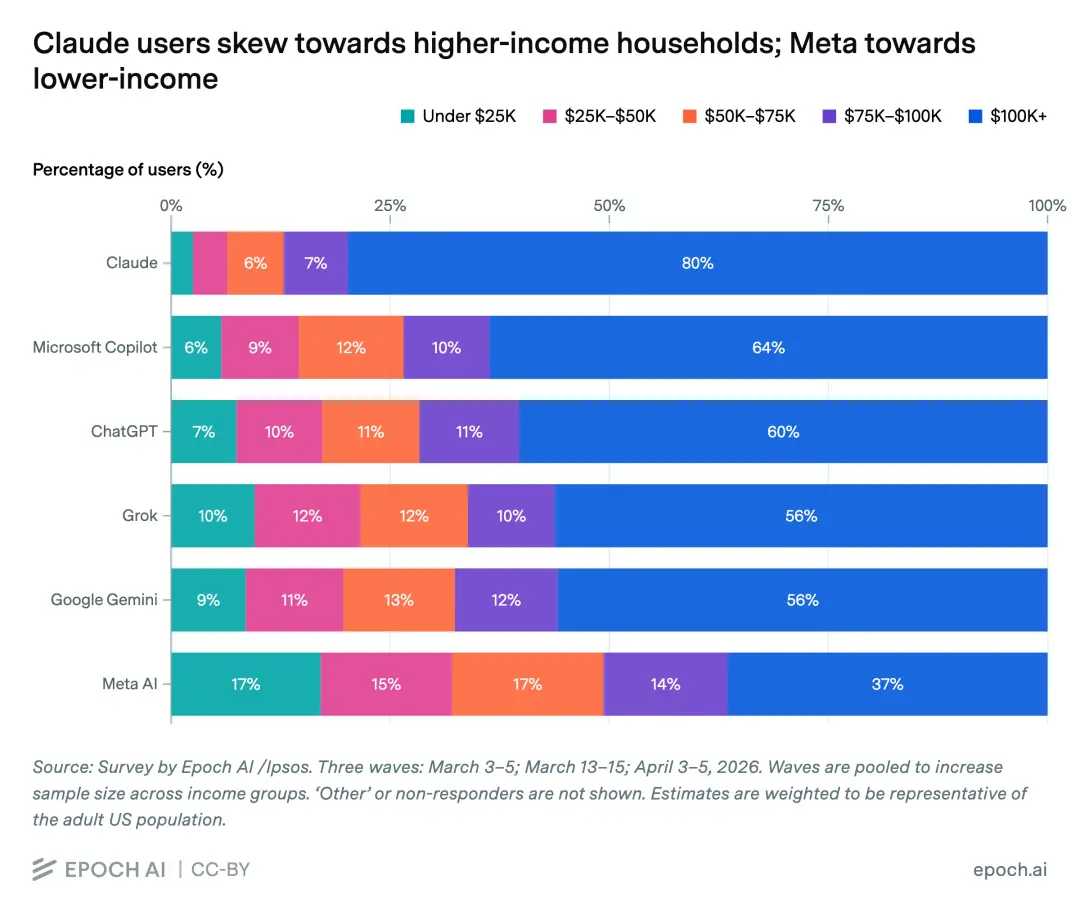

Over the past week, 79.8% of U.S. adults who have used Claude come from households with an annual income of $100,000 or more.

This proportion is higher than the 63.7% for Microsoft Copilot, 60.3% for ChatGPT, 56.2% for Grok, 55.9% for Google Gemini, and significantly higher than the 36.5% for Meta AI.

As a reference, Epoch AI estimates that approximately 50% of U.S. adults live in households with an annual income of $100,000 or more, based on U.S. Census Bureau data.

The gap at the lower income end is also significant.

Approximately 6.4% of Claude’s weekly active users come from households with an annual income of less than $50,000;

The corresponding proportion for Meta AI is 32.1%.

In the overall U.S. adult population, approximately 24% of households have an annual income of less than $50,000.

This survey was conducted in collaboration between Epoch AI and Ipsos, using Ipsos’ KnowledgePanel, a probability sample of U.S. adults based on addresses.

The first wave of the survey was conducted from March 3 to 6, 2026, with a sample size of 2,021, and a margin of error of plus or minus 2.2 percentage points at a 95% confidence level; Epoch’s subsequent analysis of income distribution also combined data from three rounds of surveys in March and April.

A more straightforward way to put it is that Claude has already shown a high income concentration in the U.S.

It hasn’t become the default entry point for the masses, but it is becoming a tool used more frequently and intensely by a certain group of people.

Claude Hasn’t Won Scale

Income profiles can easily lead to misinterpretations.

Claude’s users are wealthier, but Claude’s user base remains small.

In this national Ipsos survey, 31% of U.S. adults who used ChatGPT in the past week, 21% used Google Gemini, 11% used Microsoft Copilot, 8% used Meta AI, 5% used Grok, and only 3% used Claude.

Additionally, 49% of U.S. adults reported not having used any AI service in the past week.

The Decoder, citing Epoch AI, added another layer of data: among people with an annual income of $100,000 or more, ChatGPT’s reach is still 37%, Gemini is 24%, Copilot is 14%, and Claude is only 6%; at the same time, 44% of high-income people did not use AI services in the past week.

So, Claude’s situation is more like high income concentration, but low absolute coverage.

It appears more elite in a small pool, and is still far from approaching ChatGPT’s default status in the entire U.S. AI market.

This also explains why this data set is newsworthy.

For the past two years, AI companies have mostly used monthly active users, downloads, and call volume to tell their stories.

Now, user structure is starting to be more important than user scale.

Who is just trying it out, who is paying, and who is integrating AI into their workflow are beginning to emerge.

Why Claude?

Claude’s high-income profile is difficult to explain solely by price.

Anthropic’s Claude Pro costs $20 per month, Max 5x costs $125 per month, and Max 20x costs $250 per month. Max is aimed at users who need higher usage, fewer interruptions, and prioritized access to new models and features, and includes Claude Code.

OpenAI’s ChatGPT also has a $20 Plus plan and higher-tier Pro plans. Personal high-usage AI products are jointly entering the $100, $200 price range.

The difference lies in product perception.

ChatGPT is more like a universal entry point.

Gemini is tied to Google Search, Gmail, Docs, and other scenarios.

Copilot is more deeply connected to Microsoft 365, Word, Excel, Teams, and Edge.

Meta AI is directly integrated into WhatsApp, Instagram, Facebook, and Messenger.

Claude’s typical use cases lean more towards proactive access, long-text processing, code, complex writing, and professional tasks.

It requires users to know why they are opening it, and it is more likely to attract people who are already willing to pay for efficiency.

Ipsos’ paid subscription data also illustrates this point.

Among ChatGPT paid subscribers, 4% of respondents said they pay themselves, and 3% said their employer or school pays; the corresponding proportions for Claude are both 1%; Copilot has 5% self-paid and 10% paid by employers or schools.

Claude’s paid base is very narrow, but these people are more likely to be high-intent, high-intensity users.

This is Anthropic’s current position: small in scale, but potentially higher individual user value.

It’s not like Meta AI, which relies on social products to spread, or Google, which relies on search entry points to distribute.

Claude requires users to actively choose it.

But active choice is a barrier in itself.

Meta AI Stands on the Other End

Meta AI is on the other end of this table.

Among its weekly active users, only 36.5% come from households with an annual income of $100,000 or more, while 32.1% come from households with an annual income of less than $50,000.

Among these mainstream AI assistants, it is closest to the mass market.

The reason is not complicated.

Ipsos’ survey shows that among people who have used Meta AI, 55% accessed it through built-in features in WhatsApp, Instagram, Facebook, or Messenger, 40% saw AI-generated summaries or answers while searching on Facebook or Instagram, and only 21% went to meta.ai or the Meta AI app to ask questions.

Entry point determines users.

Meta AI is placed in social networks, Gemini is placed in search, and Copilot is placed in office software.

Claude, on the other hand, relies more on users entering the product with a clear task.

This will bring about completely different business consequences.

Meta AI can reach a wider audience, but user intent is more scattered, and many interactions may just be a casual question.

Claude has fewer users, but they are more likely to come with work problems, have clearer needs, and are more easily converted into subscriptions, API calls, or enterprise purchases.

The AI market is re-enacting the old story of the consumer internet and productivity software: one side is huge traffic entry points, and the other side is high ARPU (Average Revenue Per User) tools.

The former is responsible for coverage, and the latter is responsible for making money.

The Dividing Line is Usage Intensity

A more critical stratification occurs not only in whether or not AI is used, but also in how it is used.

Ipsos’ survey shows that among people who have used AI services in the past week, 34% used it for only one day, 49% used it for 2 to 5 days, and 16% used it almost every day.

Among the most heavy users, 62% only handled one or two quick tasks, 32% used it multiple times, and only 6% said they heavily used or relied on AI that day.

This shows that AI adoption in the U.S. already looks quite high, but most usage is still light.

Many users simply treat AI as a search box, rewriter, or temporary question-and-answer machine; a few users are starting to treat it as a work interface.

The same is true for work scenarios.

Among AI users who are employed, 46% primarily use it for personal matters, 26% primarily use it for work, and 25% use it for both work and personal use;

Among those who use AI for work, 33% use services paid for or provided by their employer, 50% use personal subscriptions or free services, and 11% use both.

This data, placed alongside Claude’s income profile, leads to a clearer judgment: the next round of competition in the AI industry is likely to revolve around high-intensity users.

High-intensity users won’t just ask about the weather, write emails, or summarize web pages.

They will integrate AI into code, contracts, sales, research, advertising, procurement, and customer service and data analysis.

The greater the gap in model capabilities, the greater the gap in the results that tools deliver.

Anthropic’s own Project Deal experiment provides an interesting piece of evidence.

In the experiment, different Claude model agents bought and sold real items in an internal market.

The stronger Opus model, as a seller, was able to sell the same item for an average of $2.68 more; as a buyer, it was able to pay an average of $2.45 less.

More subtly, users at a disadvantage did not clearly perceive that they were being taken advantage of.

This experiment is small in scale and takes place within a company, and cannot be directly extrapolated to the entire commercial world. But the direction is clear.

When AI starts to represent people in negotiations, procurement, coding, and research, model capabilities will become a new means of production.

Whoever uses the stronger model, and whoever puts the model into their workflow earlier, is likely to get better results.

The gap will be hidden in every small decision.

Signals to OpenAI, Anthropic, and Advertisers

This survey points to different issues for different companies.

For Anthropic, Claude’s high-income profile is a positive, but also a pressure.

The positive is that it proves Claude has already attracted a group of users who are more likely to pay and use it intensely.

The pressure is that Claude is still too small.

A 3% weekly usage rate does not support a mass platform narrative.

Anthropic needs to continue to increase the value of high-end users while finding more low-barrier distribution methods.

For OpenAI, ChatGPT is still the default entry point.

It leads in both overall weekly usage and reach among high-income people.

The real challenge is to convert scale advantage into higher-tier workflow lock-in, and avoid losing high-value users to Claude in scenarios such as code, research, and long documents.

For Meta, Meta AI’s lower income proportion actually shows that it is approaching the mass market.

Its commercialization path may not rely on high-priced subscriptions like Claude, but rather on extensions of advertising, recommendations, search, and content consumption entry points.

For advertisers and enterprise software companies, this is an early user map.

Different AI assistants may correspond to different purchasing power, different task types, and different conversion paths.

ChatGPT represents the largest default entry point, Claude represents higher income and more professional usage tendencies, Copilot represents enterprise distribution in office software, Gemini represents search and the Google ecosystem, and Meta AI represents mass reach in social networks.

Of course, the data should be viewed with caution.

Epoch AI notes in its income analysis that the Claude sample size is 201, and Grok is 221, compared to smaller sample sizes for ChatGPT and Gemini with wider confidence intervals;

The survey is a cross-sectional sample, and usage data is self-reported, which may have recall errors and misclassifications.

But the trend is clear enough.

AI will not only be ranked by model capabilities, but will also be re-ranked by user class, entry point, willingness to pay, and work intensity.

For the past two years, the industry has been focused on which models are stronger.

Going forward, the more valuable question will become, who is using the strongest models, who is paying for them, and who is making them part of their daily work.